As seen on the web this week...

"Ultra-loose monetary policies of recent years don’t look like they’re going to end any time soon," said Mark O’Byrne, the executive director of Dublin-based GoldCore Ltd., a brokerage that sells and stores everything from quarter-ounce British Sovereigns to 400-ounce bars. "The problems in the euro zone don’t look like they’re going to end any time soon. We’ve had a dip, and our advice to clients is always to buy the dip."

Gold Traders Get More Bullish as Central Banks Hoard More

By Nicholas Larkin -

Apr 27, 2012 12:21 PM ET

Fourteen of 28 analysts surveyed by Bloomberg expect prices to gain next week and nine were neutral, the highest proportion in two weeks. Mexico, Russia and Turkey added about 44.8 metric tons valued at $2.39 billion to reserves in March, International Monetary Fund data show. Fund managers raised their so-called net-long positions by 2.5 percent in the week ended April 17, according to the Commodity Futures Trading Commission.

Federal Reserve Chairman Ben S. Bernanke said April 25 that he’s prepared to "do more" if needed to spur the economy, and the Bank of Japan (8301) today expanded its bond-purchase plan by 10 trillion yen ($124 billion). Gold rose about 70 percent as the Fed bought $2.3 trillion of debt in two rounds of quantitative easing ending in June 2011. The U.K. fell into its first double-dip recession since the 1970s, data showed April 25, while the IMF predicts the 17-nation euro region will contract.

"Ultra-loose monetary policies of recent years don’t look like they’re going to end any time soon," said Mark O’Byrne, the executive director of Dublin-based GoldCore Ltd., a brokerage that sells and stores everything from quarter-ounce British Sovereigns to 400-ounce bars. "The problems in the euro zone don’t look like they’re going to end any time soon. We’ve had a dip, and our advice to clients is always to buy the dip."

Gold Gains Gold rose 5.7 percent to $1,656.10 an ounce this year on the Comex in New York, and is now 7.6 percent below this year’s peak. The Standard & Poor’s GSCI gauge of 24 raw materials climbed 5.8 percent as the MSCI All-Country World Index (MXWD) of equities added 9.5 percent. Treasuries gained less than 0.1 percent, a Bank of America Corp. index shows.

Options traders are also bullish, with the most widely held contract on futures traded on the Comex conferring the right to buy at $2,200 by July, 33 percent above prices now. The seven most popular options give owners the right to buy at prices ranging from $1,800 to $2,300, bourse data show.

Central banks are joining investors in buying gold, adding 439.7 tons in 2011, the most in almost five decades, the London-based World Gold Council estimates. They may buy a similar amount this year, it predicts. Mexico bought 16.8 tons last month as Russia added 16.5 tons and Turkey’s holdings expanded by 11.5 tons. Kazakhstan, Ukraine, Tajikistan and Belarus also raised reserves, according to the IMF.

Hedge Funds Speculators increased wagers on price gains to 112,275 futures and options, from a three-year low the previous week, CFTC data show. The net-long position is still 56 percent below the peak reached in August. That provides "ample room" for new long positions, Edel Tully, an analyst at UBS AG in London, wrote yesterday in a report.

Investors own 2,389.6 tons in bullion-backed exchange-traded products, within 0.9 percent of the record reached on March 13, data compiled by Bloomberg show. Demand for bullion coins is weakening, with the U.S. Mint selling 17,000 ounces so far this month, compared with an average 75,917 ounces in the previous 12 months, data on its website show.

The Fed said two days ago that growth will "pick up gradually" as the labor and housing markets show signs of improvement. About $4.99 trillion was added to the value of global equities this year on optimism the world will skirt another recession. The IMF raised its global growth outlook to 3.5 percent from 3.3 percent on April 17, while forecasting a 0.3 percent contraction in the euro area.

U.S. Recovery "If people really believe that the U.S. recovery is coming through, I think they will buy equities," said Carole Ferguson, an analyst at Fairfax IS in London. "Gold is more likely to go sideways."

Other investors may also be shunning gold. Open interest, or contracts outstanding, in U.S. futures declined to 395,389 on April 24, the lowest level since September 2009, bourse data show. That contrasts with combined open interest across the 24 commodities in the S&P GSCI, which rose 18 percent this year.

Bullion slid from a record $1,923.70 in September, taking it below the 200-day moving average, a sign of more declines to some investors. That may present a "buying opportunity,"GoldCore’s O’Byrne said. Prices held above the measure from the beginning of 2009 through the end of last year.

The metal will trade at $1,940 in 12 months, Goldman Sachs Group Inc. said in an April 24 report. The bank maintained a neutral outlook on raw materials in the near term, partly because of European debt concerns.

Benchmark Contract In other commodities, 12 of 28 traders and analysts surveyed by Bloomberg expect copper to climb next week and eight were neutral. The metal for delivery in three months, the London Metal Exchange’s benchmark contract, rose 10 percent to $8,378.25 a ton this year.

Six of 13 people surveyed said raw sugar will decline next week and three were neutral. The commodity dropped 8.9 percent this year to 21.23 cents a pound on ICE Futures U.S. in New York. Eighteen of 29 people surveyed anticipate higher corn prices next week, while 16 of 30 said soybeans will advance. Corn slipped 5.2 percent to $6.1275 a bushel this year as soybeans climbed 24 percent to $14.9175 a bushel.

"It should be the macro factors and political uncertainties that influence the markets most, and less the fundamental factors," said Daniel Briesemann, an analyst at Commerzbank AG in Frankfurt. "The sovereign debt crisis should stay in focus. I think it’s premature to say that we have seen the worst."

______________________

Central Bank gold purchases - an assessment of the impact

After yesterday's report on the latest Central Bank gold purchases, Jeffrey Nichols analyses the impact of such buying on the global gold market and its underpinning of the gold price

Author: Jeffrey Nichols

Posted: Wednesday , 25 Apr 2012

Posted: Wednesday , 25 Apr 2012

NEW YORK -

A recent survey of central-bank reserve managers predicted that the most significant change in their official reserve holdings over the next 10 years will be their intentional accumulation of gold.

In fact, central-bank reserve managers are already moving in this direction, expanding their reported bullion reserves by 439.7 tons last year - the biggest annual increase in almost five decades . . . and this doesn't count significant purchases that remain unreported.

Central banks, taking advantage of depressed market prices, were again big buyers of gold this past March according to statistics just issued by the International Monetary Fund. Reported official gold holdings increased by 49.8 metric tons last month and 55.1 tons during the first quarter.

However, it is quite likely that actual central bank gold reserves rose considerably more as some countries, led by China, choose not to report or otherwise publicize their gold market activities.

Among those central banks reporting to the IMF, Mexico was perhaps last month's most notable buyer, adding some 16.8 tons this past March on top of the 98.8 tons purchased in 2011.

Turkey added some 11.5 tons to official reserves, although this results from commercial bank transfers to meet domestic reserve and collateral requirements.

Russia, a fairly regular buyer in recent years, boosted its official gold reserves by some 15.6 tons last month and the country's central bank has said it bought another ton in the first three weeks of April. Proving itself to be an astute trader, Russia's central bank was a small seller at higher prices in February.

Kazakhstan, like Russia, buying from domestic mine production, added 4.3 tons last month. In addition, a few other countries bought smaller amounts.

Readers of my NicholsOnGold reports and followers of my more frequent Twitter posts should not be surprised by the recent news of continued significant central bank gold purchases this past March. We have repeatedly suggested that official purchases were giving the market some downside protection with central banks buying on dips when their purchases would not be disruptive or particularly visible to other market participants and observers of the gold scene.

Central banks, like many private investors, view gold as a hedge against debasement and devaluation of their U.S. dollar- and euro-denominated currency reserves.

And, because it is the only financial asset with no counterparty risk, central banks hold gold as a safe haven free from confiscatory and political risk. Indeed, both Iran and Venezuela last year, as a precaution against political risk in the form of economic sanctions, repatriated some of their official reserves that were previously held in Bank of England vaults.

With total reported global official gold reserves at roughly 31,000 tons (997 million ounces) compared to annual world gold mine output at 2,810 metric tons (about 90 million ounces), relatively small percentage changes in central bank holdings can have a significant influence on the metal's price.

In the two decades through 2009, net official sales added roughly 15 to 20 percent to the supply of gold entering the market each year. One can imagine that this additional supply had a considerable negative effect on the metal's price.

Similarly, in more recent years, the effect of central banks shifting gears - becoming net buyers rather than net sellers - has had a very positive effect on the metal's price.

I believe that net official gold accumulation will not only continue but will likely expand in 2012 and for years to come. With China and Russia leading the pack, a growing number of central banks, underweighted in gold and over-weighted in dollars and euros, will join the line to buy gold.

Importantly, the official sector will continue to underpin the price - buying on corrections when significant quantities are readily available and may be purchased discretely without disrupting the market.

Fuelling the rise in official sector interest in gold is the anticipated future depreciation of the U.S. dollar in world currency markets and the continuing erosion of its status and role as the world's key official reserve asset.

And, the dollar is not the only currency suffering a loss of respect. A few weeks ago, an Asian-country central banker told me his country's recent gold purchases had been motivated mostly by a loss of confidence in the euro as a reliable reserve asset.

In recent years, China's central bank, the People's Bank of China, has probably been the most significant buyer. Three years ago - in April 2009 - the PBOC revealed it had bought some 454 tons of gold over the preceding six years, an average of about 75 tons per year.

Since then there has been no hard evidence of additional buying . . . but my guess is that the PBOC continues to buy regularly from domestic mine production and scrap refinery output - perhaps as much as 50 to 100 tons or more per year. For its part, the PBOC not long ago said it will "seek diversification in the management of reserve assets," possibly signaling their intention to accumulate gold without actually saying so.

One day in the future we should not be surprised to see by a PBOC announcement that China's actual official gold reserves are considerably higher.

Many other central banks have also taken a much more positive view of gold in recent years. Indeed, the official sector has been a positive net buyer of gold for the past two or three years. This follows some two decades in which the official sector was a net seller of gold to the market, reflecting mostly large-scale sales by European central banks that mistakenly thought gold was in descent as a legitimate reserve asset and sold at a mere fraction of today's price.

Following many years of net annual sales in the 400-to-500 ton range, the official sector became a net buyer of gold in 2009. This is a "game changer" for the gold market. Instead of supplying hundreds of tons, year in and year out, central banks are now buying at what seems to be a net rate of 400 to 500 tons per year - representing a swing in the annual supply/demand balance of 800 to 1000 tons a year.

I don't think most market observers and participants fully appreciate just how significant this has been - and will continue to be - for the world gold market.

The list of countries that have reported gold purchases to the IMF in the past few years is itself growing with new, surprising names joining the club:

Russia has been the most outspoken and one of biggest buyers of gold in recent years. It has an explicitly stated policy to continue making monthly purchases from domestic sources at a rate of about one hundred tons a year . . . and has more than doubled its gold reserves over the past four years.

Kazakhstan is another gold-mining country intent on buying its own mine output in order to build up its official gold reserves. The National Bank of Kazakhstan has announced plans to purchase their nation's entire gold production during the next few years.

India made a strong pro-gold statement, buying 200 tons directly from the International Monetary Fund at the start of the IMF 's gold-sales program a couple of years ago.

South Korea last summer announced the purchase of 25 tons, its first purchase since 1998 when it collected and resold gold jewelry donated by patriotic citizens to help the country through a period of economic emergency.

Saudi Arabia also bought significant quantities of gold - 180 tons, in fact but did not report these purchases until last June. It is likely that the Saudi Arabia Monetary Authority continues to buy on the sly . . . along with some of the other oil producers that, like the Saudis, are over-weighted in U.S. dollar assets and grossly underweighted in gold,

Mexico was one of the biggest buyers in 2011, acquiring some 100 tons. As America's southern neighbor and close trading partner, this is yet another sign of the diminishing faith and trust in the U.S. currency.

In addition to Mexico, other recent Latin American buyers include Bolivia (which recently bought seven tons following a similar purchase in December 2010), Colombia, and Venezuela (which not only bought some gold last year, but also repatriated much of its gold reserves that were previously held abroad in the Bank of England vault),

Other names on the list of recent central-bank buyers include Thailand, Turkey, Belarus, Sri Lanka, Mauritius, and even Bangladesh.

Meanwhile, gold sales by European central banks - those that had been big sellers in the 1990s - have dwindled to practically nothing, only enough to supply their bullion and commemorative coin programs.

Keep in mind that aggregate central bank gold purchases probably exceed the official data by a wide margin.

The People's Bank of China, the Saudi Arabian Monetary Authority, and some other central banks with huge and some might say "excessive" U.S. dollar- and euro-denominated official reserve assets have an incentive to buy gold discretely and surreptitiously - simply because the announcement of their buying programs would likely boost the yellow metal's price and raise these central bank's acquisition costs.

Importantly, much of the gold bought by central banks has been bought for the long term - and will likely be held not just for a few days, weeks, months or even a few years . . . No, much of this gold will be held for decades or longer, even at much higher prices.

Central banks are now creating an upside bias to the market and are reducing the "free-float" available to meet future demand, even at much higher prices. As a consequence, we can expect less downside volatility - and a more sustainable bull market with much higher prices in the years to come.

Jeffrey Nichols is Managing Director of American Precious Metals Advisors and Senior Economic Advisor to Rosland Capital

A recent survey of central-bank reserve managers predicted that the most significant change in their official reserve holdings over the next 10 years will be their intentional accumulation of gold.

In fact, central-bank reserve managers are already moving in this direction, expanding their reported bullion reserves by 439.7 tons last year - the biggest annual increase in almost five decades . . . and this doesn't count significant purchases that remain unreported.

Central banks, taking advantage of depressed market prices, were again big buyers of gold this past March according to statistics just issued by the International Monetary Fund. Reported official gold holdings increased by 49.8 metric tons last month and 55.1 tons during the first quarter.

However, it is quite likely that actual central bank gold reserves rose considerably more as some countries, led by China, choose not to report or otherwise publicize their gold market activities.

Among those central banks reporting to the IMF, Mexico was perhaps last month's most notable buyer, adding some 16.8 tons this past March on top of the 98.8 tons purchased in 2011.

Turkey added some 11.5 tons to official reserves, although this results from commercial bank transfers to meet domestic reserve and collateral requirements.

Russia, a fairly regular buyer in recent years, boosted its official gold reserves by some 15.6 tons last month and the country's central bank has said it bought another ton in the first three weeks of April. Proving itself to be an astute trader, Russia's central bank was a small seller at higher prices in February.

Kazakhstan, like Russia, buying from domestic mine production, added 4.3 tons last month. In addition, a few other countries bought smaller amounts.

Readers of my NicholsOnGold reports and followers of my more frequent Twitter posts should not be surprised by the recent news of continued significant central bank gold purchases this past March. We have repeatedly suggested that official purchases were giving the market some downside protection with central banks buying on dips when their purchases would not be disruptive or particularly visible to other market participants and observers of the gold scene.

Central banks, like many private investors, view gold as a hedge against debasement and devaluation of their U.S. dollar- and euro-denominated currency reserves.

And, because it is the only financial asset with no counterparty risk, central banks hold gold as a safe haven free from confiscatory and political risk. Indeed, both Iran and Venezuela last year, as a precaution against political risk in the form of economic sanctions, repatriated some of their official reserves that were previously held in Bank of England vaults.

With total reported global official gold reserves at roughly 31,000 tons (997 million ounces) compared to annual world gold mine output at 2,810 metric tons (about 90 million ounces), relatively small percentage changes in central bank holdings can have a significant influence on the metal's price.

In the two decades through 2009, net official sales added roughly 15 to 20 percent to the supply of gold entering the market each year. One can imagine that this additional supply had a considerable negative effect on the metal's price.

Similarly, in more recent years, the effect of central banks shifting gears - becoming net buyers rather than net sellers - has had a very positive effect on the metal's price.

I believe that net official gold accumulation will not only continue but will likely expand in 2012 and for years to come. With China and Russia leading the pack, a growing number of central banks, underweighted in gold and over-weighted in dollars and euros, will join the line to buy gold.

Importantly, the official sector will continue to underpin the price - buying on corrections when significant quantities are readily available and may be purchased discretely without disrupting the market.

Fuelling the rise in official sector interest in gold is the anticipated future depreciation of the U.S. dollar in world currency markets and the continuing erosion of its status and role as the world's key official reserve asset.

And, the dollar is not the only currency suffering a loss of respect. A few weeks ago, an Asian-country central banker told me his country's recent gold purchases had been motivated mostly by a loss of confidence in the euro as a reliable reserve asset.

In recent years, China's central bank, the People's Bank of China, has probably been the most significant buyer. Three years ago - in April 2009 - the PBOC revealed it had bought some 454 tons of gold over the preceding six years, an average of about 75 tons per year.

Since then there has been no hard evidence of additional buying . . . but my guess is that the PBOC continues to buy regularly from domestic mine production and scrap refinery output - perhaps as much as 50 to 100 tons or more per year. For its part, the PBOC not long ago said it will "seek diversification in the management of reserve assets," possibly signaling their intention to accumulate gold without actually saying so.

One day in the future we should not be surprised to see by a PBOC announcement that China's actual official gold reserves are considerably higher.

Many other central banks have also taken a much more positive view of gold in recent years. Indeed, the official sector has been a positive net buyer of gold for the past two or three years. This follows some two decades in which the official sector was a net seller of gold to the market, reflecting mostly large-scale sales by European central banks that mistakenly thought gold was in descent as a legitimate reserve asset and sold at a mere fraction of today's price.

Following many years of net annual sales in the 400-to-500 ton range, the official sector became a net buyer of gold in 2009. This is a "game changer" for the gold market. Instead of supplying hundreds of tons, year in and year out, central banks are now buying at what seems to be a net rate of 400 to 500 tons per year - representing a swing in the annual supply/demand balance of 800 to 1000 tons a year.

I don't think most market observers and participants fully appreciate just how significant this has been - and will continue to be - for the world gold market.

The list of countries that have reported gold purchases to the IMF in the past few years is itself growing with new, surprising names joining the club:

Russia has been the most outspoken and one of biggest buyers of gold in recent years. It has an explicitly stated policy to continue making monthly purchases from domestic sources at a rate of about one hundred tons a year . . . and has more than doubled its gold reserves over the past four years.

Kazakhstan is another gold-mining country intent on buying its own mine output in order to build up its official gold reserves. The National Bank of Kazakhstan has announced plans to purchase their nation's entire gold production during the next few years.

India made a strong pro-gold statement, buying 200 tons directly from the International Monetary Fund at the start of the IMF 's gold-sales program a couple of years ago.

South Korea last summer announced the purchase of 25 tons, its first purchase since 1998 when it collected and resold gold jewelry donated by patriotic citizens to help the country through a period of economic emergency.

Saudi Arabia also bought significant quantities of gold - 180 tons, in fact but did not report these purchases until last June. It is likely that the Saudi Arabia Monetary Authority continues to buy on the sly . . . along with some of the other oil producers that, like the Saudis, are over-weighted in U.S. dollar assets and grossly underweighted in gold,

Mexico was one of the biggest buyers in 2011, acquiring some 100 tons. As America's southern neighbor and close trading partner, this is yet another sign of the diminishing faith and trust in the U.S. currency.

In addition to Mexico, other recent Latin American buyers include Bolivia (which recently bought seven tons following a similar purchase in December 2010), Colombia, and Venezuela (which not only bought some gold last year, but also repatriated much of its gold reserves that were previously held abroad in the Bank of England vault),

Other names on the list of recent central-bank buyers include Thailand, Turkey, Belarus, Sri Lanka, Mauritius, and even Bangladesh.

Meanwhile, gold sales by European central banks - those that had been big sellers in the 1990s - have dwindled to practically nothing, only enough to supply their bullion and commemorative coin programs.

Keep in mind that aggregate central bank gold purchases probably exceed the official data by a wide margin.

The People's Bank of China, the Saudi Arabian Monetary Authority, and some other central banks with huge and some might say "excessive" U.S. dollar- and euro-denominated official reserve assets have an incentive to buy gold discretely and surreptitiously - simply because the announcement of their buying programs would likely boost the yellow metal's price and raise these central bank's acquisition costs.

Importantly, much of the gold bought by central banks has been bought for the long term - and will likely be held not just for a few days, weeks, months or even a few years . . . No, much of this gold will be held for decades or longer, even at much higher prices.

Central banks are now creating an upside bias to the market and are reducing the "free-float" available to meet future demand, even at much higher prices. As a consequence, we can expect less downside volatility - and a more sustainable bull market with much higher prices in the years to come.

Jeffrey Nichols is Managing Director of American Precious Metals Advisors and Senior Economic Advisor to Rosland Capital

_______________________

Submitted by cpowell on 10:23AM ET Friday, April 27, 2012. Section: Daily Dispatches

1:20p ET Friday, April 27, 2012

Dear Friend of GATA and Gold:

Sprott Asset Management's Eric Sprott today tells King World News that the world economy is not improving, that Europeans are losing confidence in their banking system and governments, that the world's debts can be handled only through currency devaluation, and that despite price suppression efforts in the futures markets, the markets for real gold and silver will break through. An excerpt from the interview is posted at the King World News blog here:

http://kingworldnews.com/kingworldn

ews/KWN_DailyWeb/Entries/2012/4/27_Er...

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

______________________

Bill Holder on PLANET GATA [http://www.lemetropolecafe.com]

Austerity

To all; "Austerity", does anyone really believe that politicians anywhere have the stomach to follow it? You do realize that when a country goes into "austerity mode", the economy shrinks (slows) by the exact amount that the government either does not spend or raises in revenues. This is the real nuts and bolts of the entire global situation, had the governments in the U.S and Europe not printed and borrowed like drunken sailors on leave (of their senses), economic "growth" would have been "reported" far lower and or negative for years and years. I say "reported" because the current government statistics are more bogus than anything to ever be released from behind the Iron Curtain.

But back to austerity, Spain is now in the gunsights of speculators and bond vigilantes. They are REPORTING nearly 25% unemployment and the true number is most likely much much higher. Can they raise taxes? Can they tighten their belt and lay off government workers into an already unemployed populace? Can they spend less and thus "give" less to their citizens? Spain will surely be attacked in the near future and without a doubt we will hear calls for austerity. They are broke now, their banks are broke now, the time for "tightening their belt" was years and years ago when there was some "fat" in their economy that could be stored away for the lean times. The lean times are now here and they are made worse by the fact that when the good times were rolling, too much debt was accumulated to keep them rolling.

Do you see what I am talking about? Spain has NO HOPE whatsoever to extricate itself from the situation it finds itself in. They cannot grow fast enough to pay off the debt, they can't now at this point become an "austere nation", hell, they cannot even devalue their currency unless they leave the Eurozone (many will) and go forward with a devalued Peseta. I am not picking on Spain here, many other European sovereigns are in the same boat as are Britain and ultimately the U.S.. I am really bringing up Spain because the entire Western sovereign, financial and banking systems are all in the same boat, it just happens to be Spain's "turn".

The "West" which includes the US, UK, Japan. Germany and up 'til now France (amongst many others) is advocating austerity which cannot work. The funny thing is that these "black kettles" have been practising anything but austerity and continuing to run up debt. For example, in the first quarter here in the U.S., we borrowed an additional $360 Billion which "created" only $142 Billion in additional so called growth. In other words, the government borrowed (read spent) $2.50 for every Dollar that showed up as growth. In the old days before we reached "debt saturation", the Treasury sould spen $1 and get $5 or more response from the economy. Now, decreasing marginal return is an understatement. The Fed and Treasury cannot even stimulate the economy on a Dollar for Dollar basis.

So...now it appears that Europe (after Sarkozy loses) is talking about going the other way. It seems that maybe they have figured out that austerity will bring on a deflationary implosion so now it's back to what caused the problem in the first place, the overuse of debt. Europe is in the spotlight and is now acting like an out of control bobsled, bouncing back and forth off of the walls of easy money (credit) on the one side and austerity on the other. It is amazing history that we are watching.

More debt will not make old and under collateralized debt, "good" and will only lead to debasing the currencies and buying some time. Austerity will lead directly to a deflationary collapse. Up upon my soapbox again, whether these politicians figure it out or Mother Nature imposes her will, "the money" will necessarily need to be changed. The money needs to be changed and with it, a revaluation of EVERYTHING against this new money or (monies). We now sit in a system where there is around $10 Trillion worth of above ground Gold (real money) and over $1 Quadrillion of currencies and financial instruments of all sorts. Please do the math. Gold only represents 1% of the financial pyramid as it is outnumbered by well over 100-1. Included in this "100" are derivatives that 10 years ago would have been laughed at for stupidity. Now, when this inverted pyramid collapses, do you want your money as part of an "inverse floating rate 30 yr call option spread between smog carbon days and the temperature inside of a tree house in Appalachia?...Or ounces of hard money that have a history of use, value and liquidity for over 5,000 years? Either route that is (officially) chosen from here...all roads will lead to Gold. Look at the mathematical roadmap, it's pretty clear! Have a pleasant weekend and my regards, Bill H.

Gold Will Win Money War

An Open Letter to President Obama

By Christopher Barker

April 24, 2012

Submitted by cpowell on 10:23AM ET Friday, April 27, 2012. Section: Daily Dispatches

1:20p ET Friday, April 27, 2012

Dear Friend of GATA and Gold:

Sprott Asset Management's Eric Sprott today tells King World News that the world economy is not improving, that Europeans are losing confidence in their banking system and governments, that the world's debts can be handled only through currency devaluation, and that despite price suppression efforts in the futures markets, the markets for real gold and silver will break through. An excerpt from the interview is posted at the King World News blog here:

http://kingworldnews.com/kingworldn

ews/KWN_DailyWeb/Entries/2012/4/27_Er...

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

______________________

Bill Holder on PLANET GATA [http://www.lemetropolecafe.com]

Austerity

To all; "Austerity", does anyone really believe that politicians anywhere have the stomach to follow it? You do realize that when a country goes into "austerity mode", the economy shrinks (slows) by the exact amount that the government either does not spend or raises in revenues. This is the real nuts and bolts of the entire global situation, had the governments in the U.S and Europe not printed and borrowed like drunken sailors on leave (of their senses), economic "growth" would have been "reported" far lower and or negative for years and years. I say "reported" because the current government statistics are more bogus than anything to ever be released from behind the Iron Curtain.

But back to austerity, Spain is now in the gunsights of speculators and bond vigilantes. They are REPORTING nearly 25% unemployment and the true number is most likely much much higher. Can they raise taxes? Can they tighten their belt and lay off government workers into an already unemployed populace? Can they spend less and thus "give" less to their citizens? Spain will surely be attacked in the near future and without a doubt we will hear calls for austerity. They are broke now, their banks are broke now, the time for "tightening their belt" was years and years ago when there was some "fat" in their economy that could be stored away for the lean times. The lean times are now here and they are made worse by the fact that when the good times were rolling, too much debt was accumulated to keep them rolling.

Do you see what I am talking about? Spain has NO HOPE whatsoever to extricate itself from the situation it finds itself in. They cannot grow fast enough to pay off the debt, they can't now at this point become an "austere nation", hell, they cannot even devalue their currency unless they leave the Eurozone (many will) and go forward with a devalued Peseta. I am not picking on Spain here, many other European sovereigns are in the same boat as are Britain and ultimately the U.S.. I am really bringing up Spain because the entire Western sovereign, financial and banking systems are all in the same boat, it just happens to be Spain's "turn".

The "West" which includes the US, UK, Japan. Germany and up 'til now France (amongst many others) is advocating austerity which cannot work. The funny thing is that these "black kettles" have been practising anything but austerity and continuing to run up debt. For example, in the first quarter here in the U.S., we borrowed an additional $360 Billion which "created" only $142 Billion in additional so called growth. In other words, the government borrowed (read spent) $2.50 for every Dollar that showed up as growth. In the old days before we reached "debt saturation", the Treasury sould spen $1 and get $5 or more response from the economy. Now, decreasing marginal return is an understatement. The Fed and Treasury cannot even stimulate the economy on a Dollar for Dollar basis.

So...now it appears that Europe (after Sarkozy loses) is talking about going the other way. It seems that maybe they have figured out that austerity will bring on a deflationary implosion so now it's back to what caused the problem in the first place, the overuse of debt. Europe is in the spotlight and is now acting like an out of control bobsled, bouncing back and forth off of the walls of easy money (credit) on the one side and austerity on the other. It is amazing history that we are watching.

More debt will not make old and under collateralized debt, "good" and will only lead to debasing the currencies and buying some time. Austerity will lead directly to a deflationary collapse. Up upon my soapbox again, whether these politicians figure it out or Mother Nature imposes her will, "the money" will necessarily need to be changed. The money needs to be changed and with it, a revaluation of EVERYTHING against this new money or (monies). We now sit in a system where there is around $10 Trillion worth of above ground Gold (real money) and over $1 Quadrillion of currencies and financial instruments of all sorts. Please do the math. Gold only represents 1% of the financial pyramid as it is outnumbered by well over 100-1. Included in this "100" are derivatives that 10 years ago would have been laughed at for stupidity. Now, when this inverted pyramid collapses, do you want your money as part of an "inverse floating rate 30 yr call option spread between smog carbon days and the temperature inside of a tree house in Appalachia?...Or ounces of hard money that have a history of use, value and liquidity for over 5,000 years? Either route that is (officially) chosen from here...all roads will lead to Gold. Look at the mathematical roadmap, it's pretty clear! Have a pleasant weekend and my regards, Bill H.

______________________

Dave from Denver... The Golden Truth

Here's the LINK. If you only have time to read that today, stop reading this blog and read that.

On the quote at the beginning. Goldcore.com posted an essay today making the argument that one of the BRIC countries is likely to introduce a gold-backed currency at some point in the near future that will replace the dollar.

I have always believed - and I have posted my theory in the past - that China would be the likely candidate for this once it had accumulated enough gold to enable it to make the claim as having the largest gold stock in the world. The U.S. used that claim after WW2 in order to back its move to make the dollar the reserve currency per Bretton Woods.

If this does indeed occur, the dollar will likely collapse. Of course, the other interesting aspect to this would be that China/Russia would likely force the U.S. to make good on its claim that it still owns 8,100 tonnes of gold. In that regard, Mr. Wenzel from above had this point to make:

At any rate, this essay on Goldcore is another must-read: LINK, as it responds with the free market, capitalist answer to the concern that there's not enough gold in the world to make a gold standard practical. To that, the correct response is, "why not?" The value of the gold is the key variable. Value is calculated by the product of quantity and price. If the quantity is relatively fixed, and there needs to be more "value," then the price has only one way to go...

Given that enormous amount of paper fiat currency in circulation globally that has been printed up since the last time gold was used to back money, it is understandable that from a value standpoint, that the price of gold is significantly undervalued....Warren Buffet can take my last statement there and shove it up his ass.

______________________

*A Bernanke slip of the tongue while speaking Wednesday about the Fed minutes:

"Commodity prices have been well controlled over the last couple of months"

Gold market riggers don't care about being caught anymore, Embry says

Submitted by cpowell on 11:11AM ET Wednesday, April 25, 2012. Section: Daily Dispatches

2:06p ET Tuesday, April 24, 2012

Dear Friend of GATA and Gold:

Sprott Asset Management's John Embry today tells King World News that the Western gold price suppression scheme's agents are now so obvious that they don't care anymore about being caught, but the East is on to them and obtaining metal at bargain prices. An excerpt from the interview is posted at the King World News blog here:

http://kingworldnews.com/kingworldnews/KWN_Dai

lyWeb/Entries/2012/4/25_Em...

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

Shove This Up Your Ass, Warren...

Reuters’ McGeever acknowledges how the "gold market is tiny" compared to "trillions and trillions of dollars worth of cash and assets sloshing around the world financial system." He asks how can countries back "all of that" against such a "tiny and finite amount of gold?" Butler responds by saying that "the amount of gold is finite by weight or volume, it is not finite by price - article linked belowI will get to the article which is the source of the above quote below. But first I wanted to link a speech given to the NY Fed by a guy named Robert Wenzel, who authors the Economic Policy Journal blog. In this speech, he highlights the failure of Ben Bernanke's policies, why they are failing and why Government intervention in the economy leads to failure. He does a brilliant job of translating basic economic laws and theories into layman terms. With regard to the fact that Government "helps" the unemployed by taking taxpayer money and giving to the unemployed, he states rhetorically:

In present day America, the government focus has changed a bit. In the new focus, the government attempts much more to prop up the unemployed by extended payments for not working. Is it really a surprise that unemployment is so high when you pay people not to work?I've made this comment to friends and colleagues many times. He also cites work done by the recipients of the 2010 Nobe Prize in economics for work which shows that Government interference (transfer payments, regulations, etc) causes a higher rate of unemployment.

Here's the LINK. If you only have time to read that today, stop reading this blog and read that.

On the quote at the beginning. Goldcore.com posted an essay today making the argument that one of the BRIC countries is likely to introduce a gold-backed currency at some point in the near future that will replace the dollar.

I have always believed - and I have posted my theory in the past - that China would be the likely candidate for this once it had accumulated enough gold to enable it to make the claim as having the largest gold stock in the world. The U.S. used that claim after WW2 in order to back its move to make the dollar the reserve currency per Bretton Woods.

If this does indeed occur, the dollar will likely collapse. Of course, the other interesting aspect to this would be that China/Russia would likely force the U.S. to make good on its claim that it still owns 8,100 tonnes of gold. In that regard, Mr. Wenzel from above had this point to make:

I am very confused by the response of Chairman Bernanke to questioning by Congressman Ron Paul. To a seemingly near off the cuff question by Congressman Paul on Federal Reserve money provided to the Watergate burglars, Chairman Bernanke contacted the Inspector General’s Office of the Federal Reserve and requested an investigation [12]. Yet, the congressman has regularly asked about the gold certificates held by the Federal Reserve [13] and whether the gold at Fort Knox backing up the certificates will be audited. Yet there have been no requests by the Chairman to the Treasury for an audit of the gold.This I find very odd. The Chairman calls for a major investigation of what can only be an historical point of interest but fails to seek out any confirmation on a point that would be of vital interest to many present day Americans.Clearly, the gold investing community is not the only one which would be interested to see an open, legitimate, independent audit of the U.S. gold inventory - something which has not been legitimately undertaken since Eisenhower was the President. The Fed/Bernanke has jumped up and down like a lunatic promoting its new policy of "transparency." How about making good on it rather than relying on the tenuous concept of "full faith?"

In this very building, deep in the underground vaults, sits billions of dollars of gold, held by the Federal Reserve for foreign governments. The Federal Reserve gives regular tours of these vaults, even to school children. [14] Yet, America’s gold is off limits to seemingly everyone and has never been properly audited. Doesn’t that seem odd to you? If nothing else, does anyone at the Fed know the quality and fineness of the gold at Fort Knox?

At any rate, this essay on Goldcore is another must-read: LINK, as it responds with the free market, capitalist answer to the concern that there's not enough gold in the world to make a gold standard practical. To that, the correct response is, "why not?" The value of the gold is the key variable. Value is calculated by the product of quantity and price. If the quantity is relatively fixed, and there needs to be more "value," then the price has only one way to go...

Given that enormous amount of paper fiat currency in circulation globally that has been printed up since the last time gold was used to back money, it is understandable that from a value standpoint, that the price of gold is significantly undervalued....Warren Buffet can take my last statement there and shove it up his ass.

______________________

*A Bernanke slip of the tongue while speaking Wednesday about the Fed minutes:

"Commodity prices have been well controlled over the last couple of months"

Gold market riggers don't care about being caught anymore, Embry says

Submitted by cpowell on 11:11AM ET Wednesday, April 25, 2012. Section: Daily Dispatches

2:06p ET Tuesday, April 24, 2012

Dear Friend of GATA and Gold:

Sprott Asset Management's John Embry today tells King World News that the Western gold price suppression scheme's agents are now so obvious that they don't care anymore about being caught, but the East is on to them and obtaining metal at bargain prices. An excerpt from the interview is posted at the King World News blog here:

http://kingworldnews.com/kingworldnews/KWN_Dai

lyWeb/Entries/2012/4/25_Em...

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

_________________________

5 New Lies That The Federal Reserve Is Telling The American People

The Economic Collapse Blog

The Federal Reserve says that everything is going to be okay. The Fed says that unemployment is going to go down, inflation is going to remain low and economic growth is going to steadily increase. Do you believe them this time? As you will see later in this article, Federal Reserve Chairman Ben Bernanke has been dead wrong about the economy over and over again. But the mainstream media and many Americans still seem to have a lot of faith in the Federal Reserve. It doesn't seem to matter that Bernanke and other Fed officials have been telling the American people lies for years. As I always say, most people believe what they want to believe, and many people seem to want to have blind faith in the Federal Reserve even when logic and reason would dictate otherwise. The truth is that things are not going to be getting much better than they are right now. When the next wave of the financial crisis hits, the U.S. economy is going to fall back into recession, financial markets are going to crash and unemployment is going to absolutely skyrocket. But you will never hear any of that from the Federal Reserve.

The following are 5 new lies that the Federal Reserve is telling the American people. After each lie I have posted what The Economic Collapse Blog thinks is actually going to happen....

#1 The Federal Reserve says that the labor market has improved and that unemployment is going to decline significantly over the next few years.

The following is a quote from the FOMC press release that was released on Wednesday....

Labor market conditions have improved in recent months; the unemployment rate has declined but remains elevated.

The Federal Reserve is projecting that the unemployment rate will fall within the range of 7.8 percent and 8.0 percent by the end of 2012.

The Federal Reserve is also projecting that the unemployment rate will fall within the range of 6.7 percent and 7.4 percent by the end of 2014.

The Economic Collapse Blog says that the labor market has not improved. In March 2010, 58.5 percent of all working age Americans had a job. Exactly two years later in March 2012, 58.5 percent of all working age Americans had a job. If the labor market was improving, the percentage of working age Americans with a job should have gone up.

The Economic Collapse Blog also says that while there is a chance the official unemployment rate may go down slightly in the short-term, the truth is that it is going to go up into double digits once the next wave of the financial crisis hits us.

#2 The Federal Reserve says that that U.S. economy is going to experience solid GDP growth over the next couple of years.

In fact, the Federal Reserve is projecting that U.S. GDP will be rising at an annual rate that falls between 3.1 percent and 3.6 percent by the end of 2014.

The Economic Collapse Blog says that a great economic cataclysm is coming....

"When the European banking system crashes (and it will) it is going to reverberate around the globe. The epicenter of the next great financial crisis is going to be in Europe, and it is getting closer with each passing day."

#3 The Federal Reserve says that we can expect low inflation for an extended period of time.

The Federal Reserve is officially projecting that the annual rate of inflation will not be higher than 2.0 percent by the end of 2012. Federal Reserve Chairman Ben Bernanke reinforced this projection during his press conference on Wednesday....

"But we expect that to pass through the system, and assuming no new shocks in the oil sector, inflation ought to moderate to about 2 percent later this year."

The Economic Collapse Blog says that the Fed is being tremendously dishonest and that if inflation was measured the exact same way that it was measured back in 1980, the annual rate of inflation would be more than 10 percent right now.

The truth is that most middle class families know that we do not have low inflation right now. This is hammered home millions of times a day when average Americans visit the gas station or the grocery store.

At the beginning of the next recession inflation will likely subside, but that will only be because economic activity will be slowing down dramatically.

#4 The Federal Reserve says that it has built up a 30 year reputation for keeping inflation low.

Ben Bernanke actually had the gall to make the following claim during his press conference on Wednesday....

"We, the Federal Reserve, have spent 30 years building up credibility for low and stable inflation, which has proved extremely valuable in that we’ve been able to take strong accommodative actions in the last four, five years to support the economy."

Oh really?

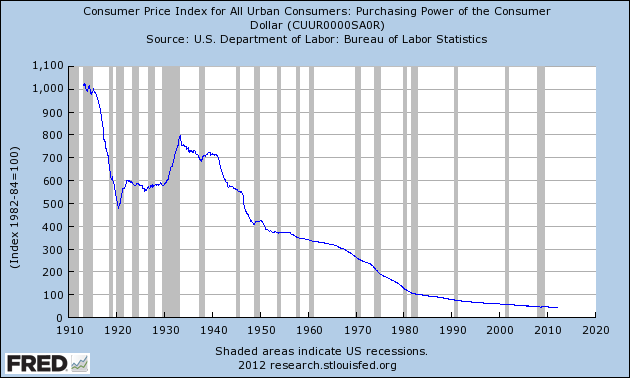

The Economic Collapse Blog says that the Federal Reserve has nearly a 100 year reputation for destroying the value of the U.S. dollar. Even using the Fed's doctored numbers, the value of the U.S. dollar has declined by more than 95 percent since 1913.

To get a really good idea of just how much the dollar has been destroyed by the Fed over the years, just check out this chart.

#5 Federal Reserve Chairman Ben Bernanke says that we should trust him because the Federal Reserve stands ready to do whatever is necessary to support the U.S. economy.

"If appropriate... we remain entirely prepared to take additional action"

The Economic Collapse Blog says that Federal Reserve Chairman Ben Bernanke is doing a great disservice by not warning the American people about the tremendous crisis that is coming. In a recent article I stated that this next crisis will blindside most Americans just like the last one did....

"Sadly, just like back in 2008, most people will never even see this next crisis coming."

So who should you trust - the Federal Reserve or all of the half-crazed bloggers out there that are warning about the "serious doom" that is coming.

Well, come back to this article in a year or two and compare how accurate the predictions were.

In the end, time will tell who is telling lies and who is not.

If we do not learn from history, we are doomed to repeat it.

For example, let's take a quick look at Ben Bernanke's track record over the past several years.

The following are statements that Bernanke actually made to the public....

#1 (July, 2005) "We’ve never had a decline in house prices on a nationwide basis. So, what I think what is more likely is that house prices will slow, maybe stabilize, might slow consumption spending a bit. I don’t think it’s gonna drive the economy too far from its full employment path, though."

#2 (October 20, 2005) "House prices have risen by nearly 25 percent over the past two years. Although speculative activity has increased in some areas, at a national level these price increases largely reflect strong economic fundamentals."

#3 (November 15, 2005) "With respect to their safety, derivatives, for the most part, are traded among very sophisticated financial institutions and individuals who have considerable incentive to understand them and to use them properly."

#4 (February 15, 2006) "Housing markets are cooling a bit. Our expectation is that the decline in activity or the slowing in activity will be moderate, that house prices will probably continue to rise."

#5 (February 15, 2007) "Despite the ongoing adjustments in the housing sector, overall economic prospects for households remain good. Household finances appear generally solid, and delinquency rates on most types of consumer loans and residential mortgages remain low."

#6 (March 28, 2007) "At this juncture, however, the impact on the broader economy and financial markets of the problems in the subprime market seems likely to be contained. In particular, mortgages to prime borrowers and fixed-rate mortgages to all classes of borrowers continue to perform well, with low rates of delinquency."

#7 (May 17, 2007) "All that said, given the fundamental factors in place that should support the demand for housing, we believe the effect of the troubles in the subprime sector on the broader housing market will likely be limited, and we do not expect significant spillovers from the subprime market to the rest of the economy or to the financial system. The vast majority of mortgages, including even subprime mortgages, continue to perform well. Past gains in house prices have left most homeowners with significant amounts of home equity, and growth in jobs and incomes should help keep the financial obligations of most households manageable."

#8 (January 10, 2008) "The Federal Reserve is not currently forecasting a recession."

#9 (June 10, 2008) "The risk that the economy has entered a substantial downturn appears to have diminished over the past month or so."

But don't worry, Ben Bernanke insists that he knows exactly what is going on this time.

So do you believe him?

A lot of Americans don't. In fact, an "economic collapse" is the number one catastrophic event that Americans worry about according to one recent survey.

Perhaps that is one reason why so many Americans are preparing for doomsday these days.

The central planners over at the Federal Reserve are not going to solve our economic problems.

The truth is that the Fed is at the very heart of our economic problems.

We have been living in the greatest debt bubble in the history of the world and that debt bubble has been facilitated by the Fed.

Over the past three decades, the total amount of debt in America has increased by about 50 trillion dollars. By stealing from future generations, we have been able to live like kings and queens, but there is going to be a great price to pay for our foolishness.

Ben Bernanke and the other folks running the Federal Reserve are just going to keep insisting that everything is going to be okay for as long as they possibly can. They are going to tell you that they know exactly how to fix things and that the economy will be back on track very soon.

Don't be stupid and believe them this time.

5 New Lies That The Federal Reserve Is Telling The American People

The Economic Collapse Blog

The Federal Reserve says that everything is going to be okay. The Fed says that unemployment is going to go down, inflation is going to remain low and economic growth is going to steadily increase. Do you believe them this time? As you will see later in this article, Federal Reserve Chairman Ben Bernanke has been dead wrong about the economy over and over again. But the mainstream media and many Americans still seem to have a lot of faith in the Federal Reserve. It doesn't seem to matter that Bernanke and other Fed officials have been telling the American people lies for years. As I always say, most people believe what they want to believe, and many people seem to want to have blind faith in the Federal Reserve even when logic and reason would dictate otherwise. The truth is that things are not going to be getting much better than they are right now. When the next wave of the financial crisis hits, the U.S. economy is going to fall back into recession, financial markets are going to crash and unemployment is going to absolutely skyrocket. But you will never hear any of that from the Federal Reserve.

The following are 5 new lies that the Federal Reserve is telling the American people. After each lie I have posted what The Economic Collapse Blog thinks is actually going to happen....

#1 The Federal Reserve says that the labor market has improved and that unemployment is going to decline significantly over the next few years.

The following is a quote from the FOMC press release that was released on Wednesday....

Labor market conditions have improved in recent months; the unemployment rate has declined but remains elevated.

The Federal Reserve is projecting that the unemployment rate will fall within the range of 7.8 percent and 8.0 percent by the end of 2012.

The Federal Reserve is also projecting that the unemployment rate will fall within the range of 6.7 percent and 7.4 percent by the end of 2014.

The Economic Collapse Blog says that the labor market has not improved. In March 2010, 58.5 percent of all working age Americans had a job. Exactly two years later in March 2012, 58.5 percent of all working age Americans had a job. If the labor market was improving, the percentage of working age Americans with a job should have gone up.

The Economic Collapse Blog also says that while there is a chance the official unemployment rate may go down slightly in the short-term, the truth is that it is going to go up into double digits once the next wave of the financial crisis hits us.

#2 The Federal Reserve says that that U.S. economy is going to experience solid GDP growth over the next couple of years.

In fact, the Federal Reserve is projecting that U.S. GDP will be rising at an annual rate that falls between 3.1 percent and 3.6 percent by the end of 2014.

The Economic Collapse Blog says that a great economic cataclysm is coming....

"When the European banking system crashes (and it will) it is going to reverberate around the globe. The epicenter of the next great financial crisis is going to be in Europe, and it is getting closer with each passing day."

#3 The Federal Reserve says that we can expect low inflation for an extended period of time.

The Federal Reserve is officially projecting that the annual rate of inflation will not be higher than 2.0 percent by the end of 2012. Federal Reserve Chairman Ben Bernanke reinforced this projection during his press conference on Wednesday....

"But we expect that to pass through the system, and assuming no new shocks in the oil sector, inflation ought to moderate to about 2 percent later this year."

The Economic Collapse Blog says that the Fed is being tremendously dishonest and that if inflation was measured the exact same way that it was measured back in 1980, the annual rate of inflation would be more than 10 percent right now.

The truth is that most middle class families know that we do not have low inflation right now. This is hammered home millions of times a day when average Americans visit the gas station or the grocery store.

At the beginning of the next recession inflation will likely subside, but that will only be because economic activity will be slowing down dramatically.

#4 The Federal Reserve says that it has built up a 30 year reputation for keeping inflation low.

Ben Bernanke actually had the gall to make the following claim during his press conference on Wednesday....

"We, the Federal Reserve, have spent 30 years building up credibility for low and stable inflation, which has proved extremely valuable in that we’ve been able to take strong accommodative actions in the last four, five years to support the economy."

Oh really?

The Economic Collapse Blog says that the Federal Reserve has nearly a 100 year reputation for destroying the value of the U.S. dollar. Even using the Fed's doctored numbers, the value of the U.S. dollar has declined by more than 95 percent since 1913.

To get a really good idea of just how much the dollar has been destroyed by the Fed over the years, just check out this chart.

#5 Federal Reserve Chairman Ben Bernanke says that we should trust him because the Federal Reserve stands ready to do whatever is necessary to support the U.S. economy.

"If appropriate... we remain entirely prepared to take additional action"

The Economic Collapse Blog says that Federal Reserve Chairman Ben Bernanke is doing a great disservice by not warning the American people about the tremendous crisis that is coming. In a recent article I stated that this next crisis will blindside most Americans just like the last one did....

"Sadly, just like back in 2008, most people will never even see this next crisis coming."

So who should you trust - the Federal Reserve or all of the half-crazed bloggers out there that are warning about the "serious doom" that is coming.

Well, come back to this article in a year or two and compare how accurate the predictions were.

In the end, time will tell who is telling lies and who is not.

If we do not learn from history, we are doomed to repeat it.

For example, let's take a quick look at Ben Bernanke's track record over the past several years.

The following are statements that Bernanke actually made to the public....

#1 (July, 2005) "We’ve never had a decline in house prices on a nationwide basis. So, what I think what is more likely is that house prices will slow, maybe stabilize, might slow consumption spending a bit. I don’t think it’s gonna drive the economy too far from its full employment path, though."

#2 (October 20, 2005) "House prices have risen by nearly 25 percent over the past two years. Although speculative activity has increased in some areas, at a national level these price increases largely reflect strong economic fundamentals."

#3 (November 15, 2005) "With respect to their safety, derivatives, for the most part, are traded among very sophisticated financial institutions and individuals who have considerable incentive to understand them and to use them properly."

#4 (February 15, 2006) "Housing markets are cooling a bit. Our expectation is that the decline in activity or the slowing in activity will be moderate, that house prices will probably continue to rise."

#5 (February 15, 2007) "Despite the ongoing adjustments in the housing sector, overall economic prospects for households remain good. Household finances appear generally solid, and delinquency rates on most types of consumer loans and residential mortgages remain low."

#6 (March 28, 2007) "At this juncture, however, the impact on the broader economy and financial markets of the problems in the subprime market seems likely to be contained. In particular, mortgages to prime borrowers and fixed-rate mortgages to all classes of borrowers continue to perform well, with low rates of delinquency."

#7 (May 17, 2007) "All that said, given the fundamental factors in place that should support the demand for housing, we believe the effect of the troubles in the subprime sector on the broader housing market will likely be limited, and we do not expect significant spillovers from the subprime market to the rest of the economy or to the financial system. The vast majority of mortgages, including even subprime mortgages, continue to perform well. Past gains in house prices have left most homeowners with significant amounts of home equity, and growth in jobs and incomes should help keep the financial obligations of most households manageable."

#8 (January 10, 2008) "The Federal Reserve is not currently forecasting a recession."

#9 (June 10, 2008) "The risk that the economy has entered a substantial downturn appears to have diminished over the past month or so."

But don't worry, Ben Bernanke insists that he knows exactly what is going on this time.

So do you believe him?

A lot of Americans don't. In fact, an "economic collapse" is the number one catastrophic event that Americans worry about according to one recent survey.

Perhaps that is one reason why so many Americans are preparing for doomsday these days.

The central planners over at the Federal Reserve are not going to solve our economic problems.

The truth is that the Fed is at the very heart of our economic problems.

We have been living in the greatest debt bubble in the history of the world and that debt bubble has been facilitated by the Fed.

Over the past three decades, the total amount of debt in America has increased by about 50 trillion dollars. By stealing from future generations, we have been able to live like kings and queens, but there is going to be a great price to pay for our foolishness.

Ben Bernanke and the other folks running the Federal Reserve are just going to keep insisting that everything is going to be okay for as long as they possibly can. They are going to tell you that they know exactly how to fix things and that the economy will be back on track very soon.

Don't be stupid and believe them this time.

_______________________

By Greg Hunter’s USAWatchdog.com

It was recently reported that countries like China and India are going to buy Iranian oil with gold. Jim Sinclair of JSMineset.com said this week, “The implications of China paying for Iranian oil in gold is the most important event in the modern history of gold.” He also said that gold could go to “$3,000 per ounce” as nations around the world revert back to gold as the only form of payment “free of liability.” (Click here to read Jim’s complete post.) There is nothing short of an epic battle quietly going on between real money (gold) and paper money (the U.S. dollar). In the end, the real thing will win out. Today, Jim Willie of GoldenJackass.com explores the battle lines and explains the global money war. Please enjoy.

———————————————————–

US Dollar VS Gold: Epic Money Battle

By: Jim Willie, Guest Writer for USAWatchdog.com

The so-called Global Financial Crisis is a term so widely used that it has earned its own acronym of GFC. When first seen, it seemed like girl friend club or some such, since many friends use GF loosely to refer to sweethearts. The GFC is falsely named, since it is more accurately described as a global monetary war with the USGovt vigorously defending its franchise in the USDollar for crude oil and trade settlement, and for bank reserves management. Take either away, and the other departs quickly, leaving the United States vulnerable to a quick ticket to the Third World marred by price inflation and supply shortage, even isolation in ring fences. On its own devices, the US is in as bad shape as the worst of the PIGS nations. The USGovt debt is above 100% of GDP finally. The annual deficit of $1.5 trillion could not be financed in normal methods. So the USFed is the adopted buyer of last resort, purchasing over 80% of new and recycled US debt issuance. The Interest Rate Swap tool acts like a hydraulic howitzer, in pushing down the long-term interest rates by creating false artificial demand. Without the IRSwap contract, a Morgan Stanley specialty, the US interest rates would be 6% to 7% just like Spain and Italy. The USTreasury Bond is not a safe haven, but rather a place where Weimar printing press operations persist, where decisions like SWIFT code rules are enforced like a illicit weapon, where billboards are painted to attract embattled investors of impaired toxic sovereign bonds from Southern Europe to retreat to the supposed safe haven of USTBonds.

WEAPON FOR INFLICTION

The USDollar has become the Weapon of Mass Self-Destruction. Three years ago, the Jackass made a statement frequently, that the first nations to depart from usage of the USDollar for exclusive trade and reserve bank operations will be the leaders in the next chapter. That list of insurgent nations is being defined right here and now. Those who remain committed to the US$ in trade and banking will put themselves at risk of systemic collapse and on a direct path on a slippery slope to the Third World. As the pace of capital destruction continues from the US$ conduit, lifting the cost structure as the debt monetization continues, the global economy will continue to falter. In the West witness the economic recession. As the USGovt raises the pressure on rebels on the world stage that refuse to comply with the USDollar Club, supported by the USMilitary that seems never to question the wisdom of directives from on high, the stress level to the entire global financial and monetary system is shaken severely. In the East witness the stall from the Western drag. The biggest blind spot among economists, whom the Jackass has unabashed bold disdain toward, has been that the ultra-low near 0% official rate has been the steady persistent cause of capital destruction and a guarantee for recession.

How tragic that economists cannot comprehend either capital formation or capital destruction under their arrogant noses! They talk of tax tweaks, of currency manipulation charges, of stimulus packages that lack effective elements, of focus on the wrong sides like consumption and retail spending. They focus on soft fluff such as inflation expectations, when the Treasury Investment Protection Securities are actually monetized by fresh money output in QE sidebar programs. No protection there! They focus on a CPI distorted to the extreme, as though it contained a shred or legitimacy. The frequent calls for more USFed bond purchases is heard, as if it is the core cure for financial market stupor. The QE bond purchases are the cancer in the body financial. The US economists are a lost bunch. The USEconomy is not the site of capitalism and economic development. It is the site of the Fascist Business Model put to practice, where preservation of large corrupted insolvent banks is given a national priority, where liquidation of insolvent broken systems such as certain financial markets and big banks is avoided at all costs. The US is the site of chronic asset collateralization and credit extension in order to support consumption to the point of systemic breakdown. Home equity raids were followed by home foreclosures, a shock to the clueless economist crew. Economists have litlte comprehension of economics, as seen by the clown hack Paul Krugman receiving a Nobel Prize. He is the absurd foppish captain of a doomed ship, elevated before its sinking. The USGovt debt, like most US State debt, like most big US bank balance sheets, like Fannie Mae debt, like AIG debt, is unsustainable, broken, in a process of collapse, all supported by the constant and high volume output of the monetary press managed by the US Federal Reserve.

Gold is becoming the Device of Financial Self-Determination, since it is free from debt and counter-party risk. The value and role of Gold has become well recognized in the last few years, especially since the financial crisis broke wide open in the summer 2007. It seems strangely obvious that Gold is money and the USDollar is not. As money flees for safety in Europe, England, and the United States, the story not told is that the monetary system is crumbling. The process has been underway since Greece broke down in December 2009, following the Dubai World debt bust. For two years, the Hat Trick Letter has been warning that Greece was simply the much smaller opening act. The real climax events in Europe would be Italy and Spain, whose government bonds are also captive wards of the Euro Central Bank state. The EuroCB acts more and more like an elite independent state, even with occasional defiance to the Germans and their Bundesbank stellar central bank, chock full of integrity, expertise, and tradition. Unfortunately, the Bundesbank signed on with the European Monetary Union as the Clydesdale horse without a side horse partner of equal strength and durability to pull the Euro stagecoach. Therefore, the ill-designed team in front steered left into the ravine. Next comes the abyss without the horse of Teutonic breed at all.

WORLDWIDE OBJECTION

The major players of the world have three major complaints on USDollar management:

1) unilateral decisions to conduct debt monetization by the USFed (debased)

2) bond fraud centered on mortgage securities, exported globally (cancer)

3) endless war with ulterior motives too numerous to specify (aggression).

The USFed never consults with victims of its monetary policy. They are scolded by them instead, after reading of the next Quantitative Easing initiative. In the real world, QE never ended. It became Global QE, appeared as Operation Twist deviously, and lately in my opinion is basically QE to Infinity. When the Dollar Swap Facility unleashed $3 trillion in loans to rescue the many broken big European banks, the impact on Chinese reserves or Brazilian reserves or Russian reserves or Korean reserves seemed very secondary and unimportant in the large scheme to preserve the USDollar Franchise system. It is breaking apart. The USFed unleashed another $2.5 trillion onto the domestic banking system, mostly to Wall Street. The debasement effect has been staggering and deeply damaging.

When obvious bond fraud in the multiple $trillions occurred, some expected justice. Not the Jackass, who noted that all prosecutions were outside Manhattan, and that within Wall Street only patsies were selected for prosecution to make an example and to establish a facade for taking firm action. The credibility of legal remedy is absent. The greater hope has centered upon the many investor lawsuits against the Wall Street banks. They will continue forever. No justice will come to the US bankers for their unprecedented white collar crime that has contributed to the systemic failure of the nation. Only with tribunals after the default.

The war front is hardly defensive in nature. It is more offensive with hidden motives. This is a delicate topic. All too often a motive has to do with preserving the USDollar usage or to obtain gold in large volume. The Libyan liberation seemed to put Qaddafi away, but the national treasury in 144 tons of gold bullion still resides in London. The conditions for its return to Libya in my view will never be met. Call my cynical, when my preference is pragmatic realist. The Iran sanctions and saber rattling are 95% about protecting the USDollar, and 5% about their nuclear refinement development. A much bigger risk was the missing former Soviet warheads, but the USGovt made no rumblings about it on the global stage 10 to 15 years ago.

GRAND BACKFIRE

The Global QE (aka QE to Infinity) put into first gear the backfire against the US. Nations around the world resented higher food, commodity, and industry input costs. On June 28th, the SWIFT bank code law goes into force to obstruct transactions. The abuse of SWIFT codes against enemies and allies alike has taken the backfire into second gear. Big strategic mistakes are being made. The G20 nations have a brain trust in the BRICS core, which has decided to pursue an alternative method of trade settlement. They describe a method to satisfy trade obligations and payments. They describe a departure from exclusive US$ settlement. They actually are working on a rival SWIFT code system from Asia, without the name. It will soon match the Western SWIFT system stride for stride in rivalry. Bigger bank centers in Asia will arise, including perhaps maritime insurance, as crippled Lloyds pulls out. Soon expect to see an Eastern SWIFT system, that China hints might be gold-backed. The main body of trade to test the new system will be on crude oil sales. The entire trade settlement system on bank payments is on the verge of a major schism, a split away from the US-dominated methods.

The several bilateral Iranian oil deals pushed the movement toward a more organization system in a backfire against the United States. The USGovt has effectively accelerated the global response to replace the USDollar in trade settlement. The misguided SWIFT weapon usage encouraged several US allies to entertain the new Eastern alternative, so that at a later date it will be embraced and used more widely. The poor chess move by the USGovt on the table sacrifices the queen. It is unclear what the next move will be to put the USDollar in checkmate. It could be a Saudi announcement to accept non-US$ for oil payments, but alongside the continued US$ usage. After all, the sand empire sitting on crude oil has new protectors in China & Russia, rendering the US a marginalized bully. The end of the Petro-Dollar will be the coup de grace for the USDollar exclusivity. The writing is more clearly written on the container vessel walls crossing the oceans than ever in the last four decades.

SHOCK & AWE INSIDE CENTRAL EUROPE